If you’re like me, you’ve probably caught yourself thinking that owning a home might simply not happen anymore. The term housing crisis doesn’t feel like a headline, but like something personal. Not in a dramatic, one-day realization kind of way. It came slowly and became a reality that looks a lot different than what you were told to expect.

You do everything right, you work, you earn, you try to save, and yet the idea of owning your own place keeps drifting further away instead of getting closer.

And the strangest part? It starts to feel normal.

Because when you actually look at what’s been happening over the past decade, the numbers don’t just tell a story, they expose a pattern. Housing prices keep climbing, aggressively and consistently, while wages move slowly, almost reluctantly, as if they’re playing an entirely different game. The gap between the two isn’t closing. It’s widening.

That’s not a coincidence. And it’s definitely not neutral.

“Housing prices are rising. Your income isn’t. That’s the problem.”

Housing crises in Europe

Let’s start with Europe.

Over the past decade, housing prices across the EU have increased by more than 50%. In some countries, it’s significantly more. Cities? Even worse.

In the last 10 years the highest increase was in Hungary (+290%), Portugal (+180%), Lithuania (+168%), and Bulgaria (+157%).

At first glance, that might sound like “normal growth.” But here’s the part that should make you stop scrolling: Wages did not follow.

Real wage growth across Europe in the same period? Roughly 10% to 30%.

That means one thing: Housing prices are rising up to 3–4 times faster than incomes.

Let that sink in.

You’re not imagining it and you’re not “bad with money.”

You’re not falling behind. The system moved ahead without you.

This isn’t inflation. It’s a gap.

People often blame inflation for rising housing costs. And yes, inflation plays a role. It pushes prices up across the economy, from food to energy to services. But traditionally, wages tend to follow, at least to some extent. Over time, salaries adjust, markets rebalance, and the system stabilizes.

What we’re seeing now doesn’t follow that pattern.

Housing prices have accelerated at a pace that far outstrips wage growth, creating a structural imbalance. It’s no longer just about things becoming more expensive. It’s about one essential part of life becoming increasingly out of reach, even for those with stable incomes.

- Housing prices: 📈 +50–60%

- Wages: 📉 +10–30%

- Affordability: 💥 collapsing

This growing disconnect is where the real pressure builds. Saving for a down payment takes significantly longer than it did a decade ago. Even households with two incomes can’t afford to buy a house or an apartment. What was once considered financially stable is starting to feel uncertain.

And that raises a deeper question.

If inflation affects the whole economy, why is housing pulling so far ahead?

Some point to supply and demand:

- not enough homes

- growing urban populations

- increased construction costs

Others highlight the role of investors, short-term rentals, and large institutions buying up property as assets rather than places to live.

Then there’s a more uncomfortable perspective.

Housing has increasingly become a financial instrument, not just a basic need. When property turns into one of the most profitable and stable investments, there is little incentive for prices to slow down. Rising values benefit those who already own assets, while making it harder for others to enter the market.

In that context, the gap isn’t accidental — it’s systemic.

It doesn’t necessarily require a coordinated effort or “control,” but it does reflect a system where access to ownership is becoming more limited over time. And when people are priced out of owning, they remain dependent on renting, loans, and long-term financial obligations.

That shift has consequences.

Because the less people own, the less financial security they have and the harder it becomes to build long-term stability.

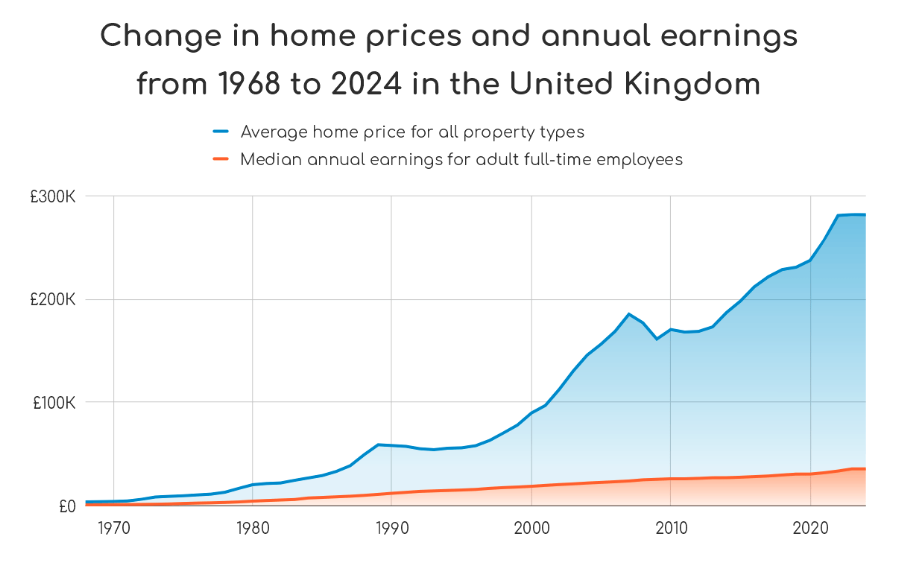

Take a look at a housing prices related to wage growth in the United Kingdom. It is absolutely terrifying.

Do you agree? Leave your thoughts in the comments.

Source: bestbrokers

The housing crisis reality for young people

Here’s what no one wants to say out loud:

Even doing everything “right” isn’t enough anymore.

- You get a degree

- You get a job

- You work full-time

- Maybe even two incomes

And still:

You can’t afford a home.

In many EU cities, buying property now requires:

- higher upfront capital

- higher debt

- longer repayment periods

And for what?

Often smaller spaces, worse locations, and more risk than a generation ago.

Why this matters more than you think

Housing is not just about having a place to live.

It’s about:

- stability

- wealth building

- long-term security

For decades, owning property was how people entered and stayed in the middle class.

Now?

That door is closing.

And once it closes, it doesn’t reopen easily.

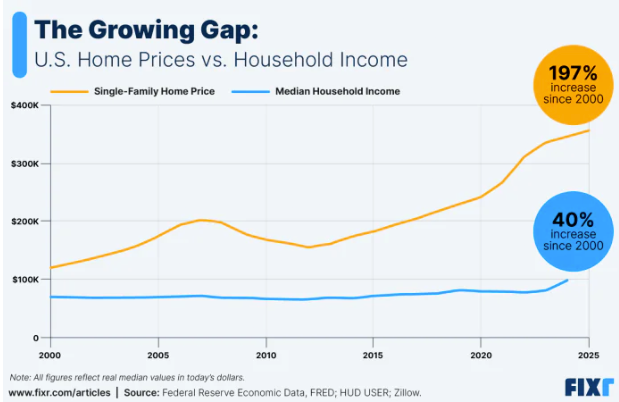

Housing prices in the U.S.: Even worse, just better packaged

If you think this is just a European issue — it’s not.

The United States is facing the same problem. In some ways, it’s even more extreme.

Source: fixr

The numbers don’t lie.

Over the past decade, housing prices per square foot have risen dramatically — from around $160 in 2014 to more than $280 in 2024. That represents roughly a 75% increase, far outpacing most other areas of the economy.

Now compare that to wages.

Median wage growth over the same period has been only around 12%. Yes, just twelve. The gap between what people earn and what they need to afford a home has widened significantly, making ownership increasingly difficult for the average person.

Let’s translate that into reality

Imagine this:

- The thing you want to buy gets 75% more expensive

- Your ability to pay for it increases by 12%

What happens?

You fall behind.

Not slowly. Rapidly.

This is why people are angry

Because the narrative doesn’t match reality.

You hear things like:

- “Just save more”

- “Cut expenses”

- “Work harder”

But the numbers tell a different story.

This isn’t about effort. It’s about structure. You cannot outwork a system where prices grow 6x faster than your income.

The psychological shift no one talks about

Something else is happening — something more subtle, but just as dangerous.

People are starting to give up.

Not loudly. Not dramatically.

Quietly.

- Delaying buying

- Staying in rentals longer

- Not even checking property listings anymore

Because what’s the point?

The middle class is getting squeezed out

This is where everything connects.

We talked about the disappearing middle class before. Housing is at the center of it. Because if you can’t own assets, you can’t build wealth.

And if you can’t build wealth, you can’t stay middle class

It’s that simple.

So what’s actually causing this housing crisis?

Quick breakdown:

1. Supply can’t keep up

Demand is rising faster than housing is being built.

2. Investors are buying homes

Not to live in — but to profit from.

3. Short-term rentals (Airbnb effect)

Homes are becoming businesses instead of living spaces.

4. Urban concentration

Everyone wants to live in the same areas.

5. Cheap money (past decade)

Low interest rates pushed prices up artificially.

None of this is random.

And none of this fixes itself.

The housing crisis truth

Let’s say it clearly. The housing crisis isn’t just something that’s randomly happening around us. It’s the result of deeper structural patterns that have been building for years. Not necessarily as part of a single, intentional plan — but as a consequence of how the system is designed.

Because when asset prices keep rising while wages remain relatively flat, the outcome is predictable. Wealth starts to concentrate in the hands of those who already own property or investments. At the same time, those trying to enter the market fall further behind with each passing year.

This isn’t just about numbers.

It’s about access. It’s about who gets to own, and who is left renting indefinitely. As the gap widens, inequality becomes visible in everyday life, from housing to financial security.

And once that gap is large enough, it becomes incredibly difficult to close.

Check out other polls on similar topics.

You’re not the problem

If you feel like:

- you’re working hard but getting nowhere

- owning a home feels out of reach

- things just don’t add up

You’re right.

They don’t.

Because:

The problem isn’t that housing prices are rising.

The problem is that your income isn’t.

And until those two lines meet again…This crisis doesn’t end.

Now it’s your turn. Tell us what you think.

Who or what is responsible for the housing crisis? Why do housing prices keep rising and wages don’t? Are we deliberately pushed into a system where owning is not possible anymore?

Leave your thoughts in the comments, vote in polls.

This is your SpeakOutZone.

Your voice. Your platform.

I’m not a doctor or a scientist. I’m a marketing professional who spent years working with health and lifestyle brands. I read a lot, ask a lot, and write about the topics that are worth debating about. My goal isn’t to tell you what to think. It’s to give you well-researched perspectives, honest opinions, and space to voice your thoughts.